Other Resources

ALL ARTICLES

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Help Center

Below you will find a number of topics ranging from personal to business banking.

.png)

For Lewis Long III, banking with Surety Bank is a relationship that has lasted more than five decades.

As one of Surety Bank's longest-standing customers, Lewis has watched the bank grow alongside the community since his connection to Surety began more than 50 years ago. He originally opened a savings account after hearing from neighbors that the bank consistently offered strong value and genuinely cared about its customers.

Over the years, Lewis has seen a lot of change. He remembers making deposits with a passbook while employees manually updated balances using a hand-cranked adding machine. What hasn't changed, however, is the way Surety Bank treats the people who walk through its doors.

For Lewis, that commitment extends beyond his own banking experience. When his sons were born, he opened accounts for each of them at Surety Bank, continuing a family tradition that has now spanned generations. One of his sons even participated in the ribbon-cutting ceremony when Surety Bank dedicated its current building in the early 1990s.

Throughout his life of military service, public service, and community involvement, Lewis has always returned to the same bank.

What has kept him loyal all these years?

The answer is simple: people.

"You couldn't ask for better service or better people," Lewis says. "I don't know how they remember everybody's name that walks in the door, but they do. They're just super folks. The people have always been a gift to us and to the community."

Lewis believes that the values Surety Bank was founded on continue to define the bank today. One story from the bank's early history has always stayed with him. During the Great Depression, he recalls hearing that Surety worked with customers rather than rushing to foreclose on them because they cared more about helping people than taking their property. That philosophy, he says, is still reflected in the way the bank serves its customers today.

It's one of the reasons Lewis has become an advocate for the bank wherever he goes.

Whether he's encouraging friends to open a money market account, sharing the bank's history, or even suggesting a new Surety branch for his hometown of Lake Helen, Lewis proudly recommends the bank he's trusted for more than half a century.

"I wouldn't champion the bank if I didn't believe in these folks and believe in this bank," he says. "Everybody is important. They see past whatever's bothering someone that day and still treat people with kindness and respect."

As Surety Bank celebrates 100 years of serving Central Florida, customers like Lewis remind us that while banking has evolved, some things should never change. Genuine relationships, exceptional service, and a commitment to the community remain at the heart of everything we do.

This is how Surety Bank has always done it. It's how we will always do it.

For 100 years, Surety Bank has believed that community banking means more than serving customers inside the walls of a branch. It means investing in the people, organizations, and partnerships that help our communities thrive.

That commitment is something Carla Quann, Director of Community Relations for the Volusia Sheriff's Office, has experienced firsthand.

"Our goal is to support everyone in our community," Carla explains. "Ryan [James] wanted to be a part of what we're doing because he cares about the community."

The partnership between Surety Bank and the Volusia Sheriff's Office began when Surety Bank President & CEO Ryan James joined the Volusia Sheriff's Foundation Board. Since then, the relationship has grown into a collaborative effort focused on addressing some of the community's greatest needs.

One example came during the holiday season, when thousands of local families faced uncertainty after SNAP benefits were unexpectedly interrupted. Through the combined efforts of businesses, volunteers, and community organizations, more than 3,500 grocery bags were distributed to families throughout Volusia County.

According to Carla, Surety Bank was an important part of making that effort possible.

Beyond community events and charitable initiatives, the partnership has also helped strengthen public safety.

As financial scams targeting older adults became increasingly common, Surety Bank worked alongside the Sheriff's Office to provide education, share industry expertise, and help detectives better recognize the warning signs of fraud.

That collaboration ultimately helped lead to the creation of the Volusia Sheriff's Office Financial Crimes Unit—a dedicated team focused on protecting residents from fraud and financial exploitation.

Working together, those efforts have helped recover more than $2 million for local victims of financial crimes.

For Carla, those results reflect what makes Surety Bank different.

"They're not just another hometown bank," she says. "They care about their community."

She believes that commitment starts with customer service but extends far beyond banking. Whether supporting nonprofit organizations, helping law enforcement address emerging scams, or simply answering the phone when someone needs help, Surety Bank has built relationships rooted in trust.

"People trust them," Carla says. "They've built that trust with their customers, and that's why people stay."

As Surety Bank celebrates a century of serving Central Florida, partnerships like this demonstrate that community banking isn't defined only by financial services—it's measured by the impact a bank has on the people and communities it serves.

For 100 years, Surety Bank has believed that when communities succeed, everyone succeeds. Through partnerships built on trust, service, and shared purpose, that commitment continues today—and will continue for generations to come.

Fraud schemes continue to evolve, and one of the latest trends affecting Money Services Businesses involves contractor-related scams. Unlike traditional check fraud, these transactions often involve legitimate cashier's checks, making them more difficult to identify through normal check verification procedures.

Instead, the focus shifts to evaluating the business behind the transaction and determining whether the overall circumstances make sense.

The scam typically begins when individuals posing as contractors approach homeowners offering services such as roofing, driveway paving, masonry work, foundation repair, or waterproofing.

These businesses often appear completely legitimate. They may have professional websites, branded clothing, business cards, invoices, and positive online reviews. In many cases, the homeowner believes they are hiring a reputable contractor.

After the work is completed, or in some cases while it is underway, the homeowner is instructed to obtain a cashier's check for payment. That check is then presented to an MSB for cashing.

The challenge is that the cashier's check itself is often valid. The fraud lies in the business behind the transaction, not the payment instrument.

Many of these businesses are created solely to facilitate the fraud. They may complete some or all of the work, but the services are often performed by unqualified labor, or left unfinished with no intention of honoring warranties or returning to correct problems.

Because the checks themselves are legitimate, identifying potential risk depends on strong corporate due diligence and careful review of the business presenting the transaction.

One of the most valuable parts of corporate due diligence is looking beyond the paperwork and evaluating whether the overall transaction makes sense.

In many of these cases, the documentation appears complete. The business may have incorporation documents, a professional website, branded materials, and everything expected during a review. On the surface, it looks legitimate.

However, taking a closer look may reveal details that deserve additional attention. For example, a construction company incorporated only days or weeks ago may already be cashing a large cashier's check for a major roofing or foundation project. While each of these facts may be reasonable on its own, together they may warrant additional review.

Consider questions such as:

No single factor indicates fraud, and every transaction should be evaluated on its own merits. However, taking a moment to consider the complete picture can help identify higher-risk transactions before they become larger issues.

This type of fraud reinforces why maintaining thorough corporate due diligence procedures is so important.

Reviewing business registrations, ownership information, supporting documentation, and overall transaction activity helps MSBs make informed decisions while reducing operational and compliance risk.

Strong due diligence is not about assuming every new business is fraudulent. It is about asking the right questions when something does not appear consistent with the overall transaction.

Fraudsters continue to refine their tactics, making scams more convincing than ever. Professional websites, polished marketing materials, and valid payment instruments should never replace thoughtful review and sound judgment.

By combining established due diligence procedures with a careful evaluation of the entire transaction, MSBs can better identify emerging fraud trends and help protect both their business and their customers.

As Surety Bank celebrates 100 years of community banking, one thing has remained constant throughout every decade: our commitment to people.

For Alexandra Wells, VP BSA Officer, that commitment is what makes community banking different.

After spending more than 20 years in the legal field, Alexandra joined Surety Bank in 2019, bringing together her legal experience and newly earned accounting degree to help protect customers from fraud, financial crimes, and suspicious activity. Since then, she has advanced through the Bank Secrecy Act department while helping strengthen Surety's commitment to customer protection. But for Alexandra, the work is about far more than regulations and risk management.

"It's about people," she says.

That philosophy became especially clear when an elderly customer began exhibiting unusual banking activity.

The customer, who had recently lost her husband and hired a caretaker, suddenly began cashing checks and making transactions that were completely out of character. Surety Bank's frontline staff noticed the changes immediately. Because they knew the customer and understood her normal banking habits, they recognized that something wasn't right.

The situation was escalated to Alexandra for further review.

After analyzing the account activity, Alexandra and another Surety employee visited the customer at her home. During the visit, several warning signs became apparent. The caretaker repeatedly answered questions on the customer's behalf, and purchases were being made that didn't align with the customer's typical behavior.

Further investigation revealed that the caretaker had gained access to the customer's debit card and was using it for personal purchases, including online shopping and vehicle rentals.

By acting quickly, Surety Bank was able to contact the customer's family, stop the unauthorized activity, and help prevent additional financial loss.

"It's one of the advantages of being a community bank," Alexandra explains. "Because we know our customers, we can recognize when something doesn't seem right and take action."

Stories like this highlight what has set Surety Bank apart for the past century. While technology and banking services continue to evolve, the foundation of community banking remains the same: relationships.

For Alexandra, those relationships extend beyond customers and into the workplace as well.

"At Surety Bank, you're not just a number," she says. "You're a person. We know each other by name, and we genuinely care about one another."

That culture of caring is reflected throughout the organization, from employees supporting one another through life's challenges to teams working together to serve customers with a personal touch.

As Surety Bank enters its second century, Alexandra believes the values that have guided the Bank for the last 100 years will continue to shape its future.

"We've always cared about our customers and our employees," she says. "That's the culture of Surety Bank, and I believe that's something that will continue for another century to come."

After 100 years, it's still how we've always done it: putting people first.

For many Money Services Businesses (MSBs), corporate due diligence files are completed during onboarding and are not reviewed on a regular basis. Over time, documents expire, registrations lapse, and required updates are overlooked.

The problem is that these files are not simply internal paperwork or a bank requirement. In many states, maintaining accurate and current corporate due diligence documentation is part of an MSB’s broader compliance responsibilities.

When documentation is incomplete or outdated, it can create operational disruptions that directly affect your business.

One of the most common issues we continue seeing involves outdated or incomplete documentation for businesses whose checks are being cashed.

In many cases, the MSB believes everything is in order until a transaction is reviewed and a problem is identified. By that point, funds may have already been provided to the customer.

When documentation is missing or expired, it can result in:

These situations are often avoidable with consistent file maintenance and regular internal reviews.

Corporate due diligence should be treated as an ongoing operational responsibility, not a one-time onboarding task.

Business information changes regularly. Companies may:

Without ongoing reviews, these changes can easily go unnoticed until they create a problem during transaction processing or compliance review.

Requirements vary depending on the state and type of business, but corporate due diligence files commonly include:

Many of these documents require periodic renewal or updates.

One recurring issue involves businesses failing to maintain active registration status with the Secretary of State.

In states like Florida, corporations are required to file annual reports to remain active. If those filings are missed, the business can become inactive or suspended.

During the due diligence process, Surety Bank reviews business registration status as part of transaction and compliance reviews. If a business is no longer active with the state, transactions may be delayed or unable to proceed until the issue is resolved.

Unfortunately, many MSBs do not discover the problem until after they have already provided funds to the customer.

One of the best ways to avoid these situations is by implementing consistent internal reviews of your corporate due diligence files.

It is recommended that MSBs review files at least twice a year to ensure documentation remains current and complete.

Even simple tracking methods can make a significant difference. Many businesses successfully use spreadsheets or internal checklists to monitor:

A small amount of organization upfront can help prevent larger operational and compliance issues later.

Corporate due diligence reviews are not simply administrative tasks. They are part of maintaining a strong compliance program and protecting your business from avoidable risk.

Strong documentation practices help businesses:

Most importantly, they help identify problems before they affect day-to-day operations.

Maintaining corporate due diligence files may not feel urgent until a transaction is delayed, a registration is found inactive, or documentation cannot be produced when needed.

Consistent reviews, updated records, and proactive tracking procedures help keep operations running smoothly and reduce preventable risk.

In many cases, the businesses with the fewest operational disruptions are simply the ones that stay organized and review their files consistently throughout the year.

For John Hamlin, business has always been about relationships.

As the owner of Hamlin & Associates and several affiliated companies, John has spent decades helping businesses succeed. Throughout his career, he's learned that the strongest partnerships aren't built on transactions alone. They're built on trust, responsiveness, and a genuine commitment to helping people when they need it most.

That's one of the reasons he's been banking with Surety Bank for nearly 20 years.

When John first moved to the Daytona Beach area, Surety Bank was recommended to him by a trusted contact. From his very first interactions with the team, he noticed something different.

"It reminded me more of an old-school bank that cared," John recalls. "I wasn't just an account number. They took the time to learn my name, understand my business, and get to know me."

Over the years, John has worked with other financial institutions, but those experiences only reinforced what makes Surety unique. While larger banks often offered similar products and technology, they couldn't provide the same level of personal attention.

"You can go anywhere and get online banking," he says. "Surety offers that too. The difference is they also offer the personal relationship."

For John, that relationship has meant having direct conversations when questions arise, receiving honest guidance, and knowing that decisions are made by people who understand both his business and his goals.

After nearly two decades as a customer, John says he's never felt the need to call and complain about an employee or a banking experience.

"Everybody in this bank is of service," he explains. "They're accommodating, they're friendly, and they're always willing to help. That's rare."

As Surety Bank celebrates its 100th anniversary, John believes the bank's longevity comes down to something simple: maintaining the personal touch while continuing to evolve.

"You guys can do everything the big banks do," he says. "They can't do everything you do."

For John, that's what community banking should be. Modern conveniences matter, but relationships matter more.

And after nearly 20 years, that's why Surety Bank continues to be his bank of choice.

This is how Surety Bank has always done it and it's how we will always do it!

For Lewis Long III, banking with Surety Bank is a relationship that has lasted more than five decades.

As one of Surety Bank's longest-standing customers, Lewis has watched the bank grow alongside the community since his connection to Surety began more than 50 years ago. He originally opened a savings account after hearing from neighbors that the bank consistently offered strong value and genuinely cared about its customers.

Over the years, Lewis has seen a lot of change. He remembers making deposits with a passbook while employees manually updated balances using a hand-cranked adding machine. What hasn't changed, however, is the way Surety Bank treats the people who walk through its doors.

For Lewis, that commitment extends beyond his own banking experience. When his sons were born, he opened accounts for each of them at Surety Bank, continuing a family tradition that has now spanned generations. One of his sons even participated in the ribbon-cutting ceremony when Surety Bank dedicated its current building in the early 1990s.

Throughout his life of military service, public service, and community involvement, Lewis has always returned to the same bank.

What has kept him loyal all these years?

The answer is simple: people.

"You couldn't ask for better service or better people," Lewis says. "I don't know how they remember everybody's name that walks in the door, but they do. They're just super folks. The people have always been a gift to us and to the community."

Lewis believes that the values Surety Bank was founded on continue to define the bank today. One story from the bank's early history has always stayed with him. During the Great Depression, he recalls hearing that Surety worked with customers rather than rushing to foreclose on them because they cared more about helping people than taking their property. That philosophy, he says, is still reflected in the way the bank serves its customers today.

It's one of the reasons Lewis has become an advocate for the bank wherever he goes.

Whether he's encouraging friends to open a money market account, sharing the bank's history, or even suggesting a new Surety branch for his hometown of Lake Helen, Lewis proudly recommends the bank he's trusted for more than half a century.

"I wouldn't champion the bank if I didn't believe in these folks and believe in this bank," he says. "Everybody is important. They see past whatever's bothering someone that day and still treat people with kindness and respect."

As Surety Bank celebrates 100 years of serving Central Florida, customers like Lewis remind us that while banking has evolved, some things should never change. Genuine relationships, exceptional service, and a commitment to the community remain at the heart of everything we do.

This is how Surety Bank has always done it. It's how we will always do it.

For 100 years, Surety Bank has believed that community banking means more than serving customers inside the walls of a branch. It means investing in the people, organizations, and partnerships that help our communities thrive.

That commitment is something Carla Quann, Director of Community Relations for the Volusia Sheriff's Office, has experienced firsthand.

"Our goal is to support everyone in our community," Carla explains. "Ryan [James] wanted to be a part of what we're doing because he cares about the community."

The partnership between Surety Bank and the Volusia Sheriff's Office began when Surety Bank President & CEO Ryan James joined the Volusia Sheriff's Foundation Board. Since then, the relationship has grown into a collaborative effort focused on addressing some of the community's greatest needs.

One example came during the holiday season, when thousands of local families faced uncertainty after SNAP benefits were unexpectedly interrupted. Through the combined efforts of businesses, volunteers, and community organizations, more than 3,500 grocery bags were distributed to families throughout Volusia County.

According to Carla, Surety Bank was an important part of making that effort possible.

Beyond community events and charitable initiatives, the partnership has also helped strengthen public safety.

As financial scams targeting older adults became increasingly common, Surety Bank worked alongside the Sheriff's Office to provide education, share industry expertise, and help detectives better recognize the warning signs of fraud.

That collaboration ultimately helped lead to the creation of the Volusia Sheriff's Office Financial Crimes Unit—a dedicated team focused on protecting residents from fraud and financial exploitation.

Working together, those efforts have helped recover more than $2 million for local victims of financial crimes.

For Carla, those results reflect what makes Surety Bank different.

"They're not just another hometown bank," she says. "They care about their community."

She believes that commitment starts with customer service but extends far beyond banking. Whether supporting nonprofit organizations, helping law enforcement address emerging scams, or simply answering the phone when someone needs help, Surety Bank has built relationships rooted in trust.

"People trust them," Carla says. "They've built that trust with their customers, and that's why people stay."

As Surety Bank celebrates a century of serving Central Florida, partnerships like this demonstrate that community banking isn't defined only by financial services—it's measured by the impact a bank has on the people and communities it serves.

For 100 years, Surety Bank has believed that when communities succeed, everyone succeeds. Through partnerships built on trust, service, and shared purpose, that commitment continues today—and will continue for generations to come.

Fraud schemes continue to evolve, and one of the latest trends affecting Money Services Businesses involves contractor-related scams. Unlike traditional check fraud, these transactions often involve legitimate cashier's checks, making them more difficult to identify through normal check verification procedures.

Instead, the focus shifts to evaluating the business behind the transaction and determining whether the overall circumstances make sense.

The scam typically begins when individuals posing as contractors approach homeowners offering services such as roofing, driveway paving, masonry work, foundation repair, or waterproofing.

These businesses often appear completely legitimate. They may have professional websites, branded clothing, business cards, invoices, and positive online reviews. In many cases, the homeowner believes they are hiring a reputable contractor.

After the work is completed, or in some cases while it is underway, the homeowner is instructed to obtain a cashier's check for payment. That check is then presented to an MSB for cashing.

The challenge is that the cashier's check itself is often valid. The fraud lies in the business behind the transaction, not the payment instrument.

Many of these businesses are created solely to facilitate the fraud. They may complete some or all of the work, but the services are often performed by unqualified labor, or left unfinished with no intention of honoring warranties or returning to correct problems.

Because the checks themselves are legitimate, identifying potential risk depends on strong corporate due diligence and careful review of the business presenting the transaction.

One of the most valuable parts of corporate due diligence is looking beyond the paperwork and evaluating whether the overall transaction makes sense.

In many of these cases, the documentation appears complete. The business may have incorporation documents, a professional website, branded materials, and everything expected during a review. On the surface, it looks legitimate.

However, taking a closer look may reveal details that deserve additional attention. For example, a construction company incorporated only days or weeks ago may already be cashing a large cashier's check for a major roofing or foundation project. While each of these facts may be reasonable on its own, together they may warrant additional review.

Consider questions such as:

No single factor indicates fraud, and every transaction should be evaluated on its own merits. However, taking a moment to consider the complete picture can help identify higher-risk transactions before they become larger issues.

This type of fraud reinforces why maintaining thorough corporate due diligence procedures is so important.

Reviewing business registrations, ownership information, supporting documentation, and overall transaction activity helps MSBs make informed decisions while reducing operational and compliance risk.

Strong due diligence is not about assuming every new business is fraudulent. It is about asking the right questions when something does not appear consistent with the overall transaction.

Fraudsters continue to refine their tactics, making scams more convincing than ever. Professional websites, polished marketing materials, and valid payment instruments should never replace thoughtful review and sound judgment.

By combining established due diligence procedures with a careful evaluation of the entire transaction, MSBs can better identify emerging fraud trends and help protect both their business and their customers.

For John Hamlin, business has always been about relationships.

As the owner of Hamlin & Associates and several affiliated companies, John has spent decades helping businesses succeed. Throughout his career, he's learned that the strongest partnerships aren't built on transactions alone. They're built on trust, responsiveness, and a genuine commitment to helping people when they need it most.

That's one of the reasons he's been banking with Surety Bank for nearly 20 years.

When John first moved to the Daytona Beach area, Surety Bank was recommended to him by a trusted contact. From his very first interactions with the team, he noticed something different.

"It reminded me more of an old-school bank that cared," John recalls. "I wasn't just an account number. They took the time to learn my name, understand my business, and get to know me."

Over the years, John has worked with other financial institutions, but those experiences only reinforced what makes Surety unique. While larger banks often offered similar products and technology, they couldn't provide the same level of personal attention.

"You can go anywhere and get online banking," he says. "Surety offers that too. The difference is they also offer the personal relationship."

For John, that relationship has meant having direct conversations when questions arise, receiving honest guidance, and knowing that decisions are made by people who understand both his business and his goals.

After nearly two decades as a customer, John says he's never felt the need to call and complain about an employee or a banking experience.

"Everybody in this bank is of service," he explains. "They're accommodating, they're friendly, and they're always willing to help. That's rare."

As Surety Bank celebrates its 100th anniversary, John believes the bank's longevity comes down to something simple: maintaining the personal touch while continuing to evolve.

"You guys can do everything the big banks do," he says. "They can't do everything you do."

For John, that's what community banking should be. Modern conveniences matter, but relationships matter more.

And after nearly 20 years, that's why Surety Bank continues to be his bank of choice.

This is how Surety Bank has always done it and it's how we will always do it!

For John Simmons, banking with Surety has always been about relationships.

A longtime customer of Surety Bank, John has seen firsthand what it looks like when a financial institution truly shows up for its community. As a husband of 38 years, a father of four daughters, and a Director at St. Barnabas Episcopal School, his perspective is grounded in both family and service.

When the school began to grow, a new challenge emerged. They had run out of space to fit all of the students. Expansion wasn’t just a nice-to-have, it was necessary to continue serving students and families well. Like many organizations in that position, they explored their options carefully.

Then came a call that changed everything.

The president of Surety Bank reached out directly, bringing together key stakeholders in a conversation focused on one thing: how to help. What followed was more than a transaction, it was a collaborative effort. The bank stepped in not just with financial guidance, but with a clear commitment to walk alongside the school’s leadership every step of the way.

That experience left a lasting impression on John.

In his words, Surety Bank was “there 120%,” offering direction, support, and reassurance during a critical moment. But what stood out most was how they got there.

“They treat people as people,” John explains. “They actually answer the phone. They communicate.”

In an era where many businesses prioritize efficiency over connection, that kind of responsiveness feels increasingly rare. Yet for Surety Bank, it’s part of their DNA.

John’s story is a reminder that the best banking relationships aren’t built on numbers alone. They’re built on trust, accessibility, and a genuine investment in the people they serve.

This is how Surety Bank has always done it and it’s how we will always do it!

As Surety Bank celebrates 100 years of community banking, one thing has remained constant throughout every decade: our commitment to people.

For Alexandra Wells, VP BSA Officer, that commitment is what makes community banking different.

After spending more than 20 years in the legal field, Alexandra joined Surety Bank in 2019, bringing together her legal experience and newly earned accounting degree to help protect customers from fraud, financial crimes, and suspicious activity. Since then, she has advanced through the Bank Secrecy Act department while helping strengthen Surety's commitment to customer protection. But for Alexandra, the work is about far more than regulations and risk management.

"It's about people," she says.

That philosophy became especially clear when an elderly customer began exhibiting unusual banking activity.

The customer, who had recently lost her husband and hired a caretaker, suddenly began cashing checks and making transactions that were completely out of character. Surety Bank's frontline staff noticed the changes immediately. Because they knew the customer and understood her normal banking habits, they recognized that something wasn't right.

The situation was escalated to Alexandra for further review.

After analyzing the account activity, Alexandra and another Surety employee visited the customer at her home. During the visit, several warning signs became apparent. The caretaker repeatedly answered questions on the customer's behalf, and purchases were being made that didn't align with the customer's typical behavior.

Further investigation revealed that the caretaker had gained access to the customer's debit card and was using it for personal purchases, including online shopping and vehicle rentals.

By acting quickly, Surety Bank was able to contact the customer's family, stop the unauthorized activity, and help prevent additional financial loss.

"It's one of the advantages of being a community bank," Alexandra explains. "Because we know our customers, we can recognize when something doesn't seem right and take action."

Stories like this highlight what has set Surety Bank apart for the past century. While technology and banking services continue to evolve, the foundation of community banking remains the same: relationships.

For Alexandra, those relationships extend beyond customers and into the workplace as well.

"At Surety Bank, you're not just a number," she says. "You're a person. We know each other by name, and we genuinely care about one another."

That culture of caring is reflected throughout the organization, from employees supporting one another through life's challenges to teams working together to serve customers with a personal touch.

As Surety Bank enters its second century, Alexandra believes the values that have guided the Bank for the last 100 years will continue to shape its future.

"We've always cared about our customers and our employees," she says. "That's the culture of Surety Bank, and I believe that's something that will continue for another century to come."

After 100 years, it's still how we've always done it: putting people first.

Fraud schemes continue to evolve, and one of the latest trends affecting Money Services Businesses involves contractor-related scams. Unlike traditional check fraud, these transactions often involve legitimate cashier's checks, making them more difficult to identify through normal check verification procedures.

Instead, the focus shifts to evaluating the business behind the transaction and determining whether the overall circumstances make sense.

The scam typically begins when individuals posing as contractors approach homeowners offering services such as roofing, driveway paving, masonry work, foundation repair, or waterproofing.

These businesses often appear completely legitimate. They may have professional websites, branded clothing, business cards, invoices, and positive online reviews. In many cases, the homeowner believes they are hiring a reputable contractor.

After the work is completed, or in some cases while it is underway, the homeowner is instructed to obtain a cashier's check for payment. That check is then presented to an MSB for cashing.

The challenge is that the cashier's check itself is often valid. The fraud lies in the business behind the transaction, not the payment instrument.

Many of these businesses are created solely to facilitate the fraud. They may complete some or all of the work, but the services are often performed by unqualified labor, or left unfinished with no intention of honoring warranties or returning to correct problems.

Because the checks themselves are legitimate, identifying potential risk depends on strong corporate due diligence and careful review of the business presenting the transaction.

One of the most valuable parts of corporate due diligence is looking beyond the paperwork and evaluating whether the overall transaction makes sense.

In many of these cases, the documentation appears complete. The business may have incorporation documents, a professional website, branded materials, and everything expected during a review. On the surface, it looks legitimate.

However, taking a closer look may reveal details that deserve additional attention. For example, a construction company incorporated only days or weeks ago may already be cashing a large cashier's check for a major roofing or foundation project. While each of these facts may be reasonable on its own, together they may warrant additional review.

Consider questions such as:

No single factor indicates fraud, and every transaction should be evaluated on its own merits. However, taking a moment to consider the complete picture can help identify higher-risk transactions before they become larger issues.

This type of fraud reinforces why maintaining thorough corporate due diligence procedures is so important.

Reviewing business registrations, ownership information, supporting documentation, and overall transaction activity helps MSBs make informed decisions while reducing operational and compliance risk.

Strong due diligence is not about assuming every new business is fraudulent. It is about asking the right questions when something does not appear consistent with the overall transaction.

Fraudsters continue to refine their tactics, making scams more convincing than ever. Professional websites, polished marketing materials, and valid payment instruments should never replace thoughtful review and sound judgment.

By combining established due diligence procedures with a careful evaluation of the entire transaction, MSBs can better identify emerging fraud trends and help protect both their business and their customers.

For many Money Services Businesses (MSBs), corporate due diligence files are completed during onboarding and are not reviewed on a regular basis. Over time, documents expire, registrations lapse, and required updates are overlooked.

The problem is that these files are not simply internal paperwork or a bank requirement. In many states, maintaining accurate and current corporate due diligence documentation is part of an MSB’s broader compliance responsibilities.

When documentation is incomplete or outdated, it can create operational disruptions that directly affect your business.

One of the most common issues we continue seeing involves outdated or incomplete documentation for businesses whose checks are being cashed.

In many cases, the MSB believes everything is in order until a transaction is reviewed and a problem is identified. By that point, funds may have already been provided to the customer.

When documentation is missing or expired, it can result in:

These situations are often avoidable with consistent file maintenance and regular internal reviews.

Corporate due diligence should be treated as an ongoing operational responsibility, not a one-time onboarding task.

Business information changes regularly. Companies may:

Without ongoing reviews, these changes can easily go unnoticed until they create a problem during transaction processing or compliance review.

Requirements vary depending on the state and type of business, but corporate due diligence files commonly include:

Many of these documents require periodic renewal or updates.

One recurring issue involves businesses failing to maintain active registration status with the Secretary of State.

In states like Florida, corporations are required to file annual reports to remain active. If those filings are missed, the business can become inactive or suspended.

During the due diligence process, Surety Bank reviews business registration status as part of transaction and compliance reviews. If a business is no longer active with the state, transactions may be delayed or unable to proceed until the issue is resolved.

Unfortunately, many MSBs do not discover the problem until after they have already provided funds to the customer.

One of the best ways to avoid these situations is by implementing consistent internal reviews of your corporate due diligence files.

It is recommended that MSBs review files at least twice a year to ensure documentation remains current and complete.

Even simple tracking methods can make a significant difference. Many businesses successfully use spreadsheets or internal checklists to monitor:

A small amount of organization upfront can help prevent larger operational and compliance issues later.

Corporate due diligence reviews are not simply administrative tasks. They are part of maintaining a strong compliance program and protecting your business from avoidable risk.

Strong documentation practices help businesses:

Most importantly, they help identify problems before they affect day-to-day operations.

Maintaining corporate due diligence files may not feel urgent until a transaction is delayed, a registration is found inactive, or documentation cannot be produced when needed.

Consistent reviews, updated records, and proactive tracking procedures help keep operations running smoothly and reduce preventable risk.

In many cases, the businesses with the fewest operational disruptions are simply the ones that stay organized and review their files consistently throughout the year.

.jpg)

For many Money Services Businesses (MSBs), the independent review is viewed as another annual compliance requirement to complete, submit to the bank, and move on from until next year.

In reality, the independent review is one of the most important tools available to help identify weaknesses in your compliance program before they become larger problems.

A completed review alone is not enough.

What matters is what happens after the review is finished.

Independent testing is one of the pillars of an effective BSA/AML compliance program. Its purpose is not simply to satisfy a requirement. A quality review evaluates the strength of your compliance program, identifies weaknesses or gaps, reviews transaction monitoring procedures, and provides recommendations to improve controls and reduce risk.

A strong independent review gives MSB owners visibility into areas that may need attention before regulators or financial institutions identify them first.

One of the biggest issues we see is MSBs treating the independent review as a one-time document instead of an operational tool.

In many cases, findings are not addressed, recommendations are delayed, or the same deficiencies continue appearing year after year. This creates a pattern that signals a lack of improvement and a lack of attention to compliance responsibilities.

When the same issues continue repeating, risk increases significantly.

Repeated deficiencies can eventually lead to increased monitoring requirements, additional compliance costs, regulatory scrutiny, or even fines and penalties. In more serious situations, it can also create risk for the MSB’s banking relationship or licensing status.

In some cases, businesses may be required to undergo additional compliance monitoring by an outside third party until improvements are made.

The goal is not to create an additional burden, but instead to identify and correct issues before they become larger operational or regulatory problems.

Independent reviews frequently identify issues involving:

While some of these may seem minor individually, repeated deficiencies over time can create significant compliance concerns if they are not corrected.

No compliance program is perfect. What matters most is identifying issues, addressing them promptly, and demonstrating improvement over time.

An independent review should show progress year after year. If the same findings continue appearing without corrective action, regulators and financial institutions may view that as a lack of commitment to compliance obligations.

Although the independent review report is a bank-required document, MSBs are required to undergo independent testing because the Bank Secrecy Act (BSA) requires every MSB to maintain an effective Anti-Money Laundering (AML) program, and independent testing is one of the core required elements of that program.

While FinCEN requires independent testing to be conducted periodically, Surety Bank’s policy requires independent testing to be completed every 12 months for MSB customers.

Completing reviews consistently and addressing findings in a timely manner helps maintain a stronger and more effective compliance program throughout the year.

Compliance is not built once a year during an independent testing. It is built through consistent attention to processes, documentation, monitoring, and corrective action throughout the year.

The independent testing is designed to help identify weaknesses before they create larger operational or regulatory problems. Using it properly can help protect your business, your banking relationship, and your long-term success.

Not all risks come from outside your business.

In many cases, the most significant issues we see develop internally through gaps in oversight, compliance, and day-to-day controls.

As we move further into the year, we want to focus on a key principle that helps prevent these issues:

Trust your team, but verify your operations.

Consider the following scenario:

An MSB owner invested in the business but was not involved in day-to-day operations. Instead, they trusted a close family member to manage the store and handle compliance responsibilities.

At first, everything appeared to be running smoothly.

Over time, however, several issues developed:

Eventually, the situation escalated.

The individual managing the business began making unauthorized financial decisions. There were compliance gaps that had gone unnoticed. Required oversight was missing. By the time the issues surfaced, the impact included:

The most important takeaway is this:

The responsibility did not fall on the person running the store. It fell on the owner.

Even if you assign:

The responsibility for compliance, licensing, and operations remains with the owner.

Regulators evaluate the licensed entity and the owner behind it, not just the individual performing the work.

A “hands-off” approach can create risk if there is no system in place to verify what is happening inside the business.

Internal issues are not always obvious.

Unlike external fraud, which is often a single event, internal breakdowns can develop gradually:

Because the business appears to be operating normally, these issues can go unnoticed until they become serious.

Oversight does not mean mistrust. It means protection.

Strong MSB operations include:

Owners do not need to manage every transaction, but they do need visibility into how the business is operating.

To reduce risk and strengthen your operation, consider:

Even small, consistent actions can help identify issues early.

Independent reviews, compliance officers, and internal staff all play important roles.

However, none of these replace owner oversight.

If any one layer fails, there should be another layer in place to identify and correct the issue.

Trust is important in any business. But in an MSB environment, trust must be supported by structure, process, and verification.

A strong system protects:

If you have questions about internal controls, compliance expectations, or how to strengthen oversight in your business, our team is available to support you.

.jpg)

Tax season often brings an increase in check fraud activity, and we are currently seeing specific patterns in several markets. Based on recent site visits and bankwide data, fraud trends include altered checks, fraudulent IDs, and tax refund schemes that can put MSBs at risk.

Fraud is not evenly distributed across the country. Recent analysis shows:

Understanding these localized trends can help MSBs tailor their detection and prevention efforts based on where their business operates.

Why Fraud Is Often Missed

In busy MSB settings, tellers and staff are under pressure to process customers quickly. Fast service is important, but it should not come at the expense of proper verification. Common reasons fraud is missed include:

Slowing down when suspicious signals appear can prevent significant losses later.

One of the most common fraud methods involves chemical alteration (sometimes called “check washing”), where fraudsters remove original payee information and rewrite it.

How to detect it:

Areas that glow differently often indicate tampering.

Even if the check has no embedded security feature, an altered area will reflect under UV light in a way that the original paper will not.

Fraud prevention is not only about tools. People exhibit behavior that often signals something is wrong:

Watch for customers who:

These behaviors, when combined with instrument anomalies, are stronger indicators of fraud.

In some cases, the check is real, but the transaction context is not. A common example seen in Michigan:

These patterns suggest the check itself may be authentic, but the process that generated it was fraudulent. The bank will eventually identify the issue, but MSBs may face loss if the check is returned.

Slowing down and asking questions helps you protect your business from future exposure.

It’s natural to want to avoid losing a small fee by turning away a suspicious check. However, a rushed decision can expose your business to a much higher loss when a check is returned or fails later verification.

Protecting your business means:

When fraud is prevented at the front line, the long-term financial health of your business is protected.

For cash-heavy businesses, deposit routines are not just an operations detail. They are a security issue, a controls issue, and often a cash-flow issue. When business cash gets deposited “personally,” meaning an owner or employee deposits cash through personal banking habits or into the wrong account, it can blur your recordkeeping and weaken internal controls. The IRS notes it is a good idea to keep separate business and personal accounts because it makes recordkeeping easier. The U.S. Small Business Administration also emphasizes separating funds by using a dedicated business bank account to keep bookkeeping clean and accurate.

Just as important is the security perspective. Regularly sending someone to the bank with cash exposes employees to real risk, and it creates a predictable pattern that can be exploited. The ABA Banking Journal has noted that too many cash-handling touch points, including trips to the bank, increase risk and can put employees in physical danger. Brink’s similarly points out that employees are exposed to theft risk when transporting cash, and that partnering with trained cash logistics professionals can reduce the risk of theft and increase accountability through secure transport procedures.

Some businesses try to replace bank runs with a courier pickup, but not every courier model is designed for cash. Cash transportation is high-risk, and the best solution is typically a purpose-built cash logistics provider whose job is secure cash handling, documentation, and transport. Trained cash logistics professionals and armored services are structured to reduce theft exposure and strengthen chain-of-custody and accountability, which is fundamentally different from general delivery services.

Surety Bank’s Smart Safe is designed specifically for cash-heavy businesses that want stronger security and a cleaner, more reliable deposit process. Surety explains that, through its partnership with Loomis, Smart Safe lets your business deposit cash on-site, receive provisional credit to your Surety Bank account, and eliminate unnecessary bank runs. From a security standpoint, Surety highlights benefits like real-time tracking of deposits, enhanced security for cash and employees, and better accountability with fewer cash shortages.

From a cash-flow standpoint, Surety’s process is built around speed. You enter the amount, deposit the cash into the Smart Safe device, and Surety provides provisional credit to your business account based on that entry. Loomis also describes provisional credit as daily credit for cash deposits without having to go to the bank, reducing time and helping reduce the risk of robbery outside the store.

If your business handles cash, the goal is to reduce handling, reduce trips, and reduce uncertainty. A strong plan usually includes keeping all business cash activity in business accounts and processes with clear documentation and daily reconciliation, minimizing manual bank runs, and using a Smart Safe with a professional cash logistics partner so deposits are tracked and transport is handled by specialists.

Contact our Treasury Services department today to learn how Smart Safe can help you strengthen security, simplify deposits, and improve visibility into your cash.

This is the first of a new series of fictional case study articles. The business principles are applicable to all industries, not just the industry mentioned below.

Mike had spent years building his commercial construction company from the ground up. He took pride in his work, bidding on high-profile projects and assembling what he thought was a solid team. But as his company grew, so did his hiring challenges—especially when it came to leadership positions.

One project in particular—a multi-million dollar office complex—pushed his business to the edge. Under pressure to meet deadlines, Mike rushed to hire a new project manager, Tom, who came with an impressive résumé and glowing recommendations. But within weeks, cracks began to show.

Tom cut corners, ordered cheaper materials to save costs (without approval), and ignored safety protocols. Worse, he treated crew members poorly, causing skilled workers to quit mid-project. By the time Mike caught on, the damage was done. The project was behind schedule, client trust had eroded, and fixing Tom’s mistakes cost the company thousands.

Determined not to repeat the mistake, Mike changed his hiring approach. He thoroughly vetted new hires, conducted trial periods for leadership roles, and built a workplace culture that rewarded integrity and reliability. Within a year, his company had a team of dedicated leaders who took pride in their work—and it showed in their projects.

For businesses like Mike’s, hiring the right leadership isn’t just about filling roles—it’s about protecting the company's reputation, profitability, and long-term success.

A business can only succeed if its leadership is competent, ethical, and aligned with company values. A poor leadership hire can derail entire teams, weaken morale, and ultimately cost the company in lost productivity and damaged relationships.

The problem isn’t just finding someone with the right credentials. Many executives, managers, and directors look great on paper but fail to lead effectively. Worse, some take advantage of their positions, making decisions that benefit themselves at the expense of the company.

Avoiding these pitfalls requires a thoughtful hiring strategy that goes beyond skills and experience to assess character, leadership style, and long-term commitment.

When hiring for leadership roles, businesses should focus on finding ethical, capable, and accountable individuals. Here’s how:

Even the best leadership hire won’t stick around if they feel undervalued or unsupported. To keep strong leaders, businesses should:

Hiring and retaining the right leaders is just as critical—if not more so—than hiring the right employees. Leaders set the tone for company culture, influence productivity, and ultimately determine business success.

If your company has struggled with hiring leadership roles, it’s time to refine your hiring process, emphasize integrity, and invest in leadership development. By learning from mistakes—like Mike did—and implementing better hiring and retention practices, businesses can build a team of strong, ethical leaders who drive long-term success.

For more pratical information on hiring for a leadership position, check out this recent episode of the Expandable Show. https://www.youtube.com/watch?v=NtRezs5v4oA

In this article we want to answer the major questions surrounding proper employee training so you can use this as a tool to improve the performance of your business.

Why you should train your employees

Most mistakes that MSBs make in their businesses are directly related to their lack of employee training.

Many mistakes can be avoided, and your business doesn’t have to suffer by being held back. But it takes a little bit of time and energy invested into best practices to create an environment that is geared towards training.

We see some MSBs focusing their time and attention in other places too often which leaves their employees unsure about how to handle certain situations. The result can come in the form of fines, slowed growth, losing your MSB license and even losing their banking relationship.

Another major reason to train employees is to fully utilize your resources and assets. For example, you are using a software for check cashing. Are you using just the surface level features or are you using it to its fullest potential? This software offers a lot of features that can make your employees’ jobs much easier and can create efficiencies that map to profitability. This asset alone could bring improvements that impact your business tremendously in the short and long term.

Employee training should be held as a high priority and taken seriously. If so, the result is a smooth operation, less drag on resources and time spent fixing mistakes and less worry about being in business in the coming months or years.

Taking employee training seriously is the first step to sustainable growth in your MSB business. It’s the foundation of everything you do and the bedrock of your business.

How to train your employees

One of the four pillars of BSA is required employee training.

Naturally, if training is not considered a high priority in your business, employees will find ways to fulfill this requirement without becoming more knowledgeable or getting better in their role. People are generally going to take the path of least resistance when it is offered to them unless you are creating an environment with a higher standard.

Taking a basic test online to fulfill training requirements isn’t always going to achieve the desired result. You’re not doing training just to say you completed it. The purpose of completing the training is to stay compliant, get better and avoid costly mistakes that can put you out of business.

Besides completing a standardized test to confirm your knowledge of the subject, employee training best practices include several other factors. We’ve listed some of them here.

Stay up to speed on current events that are happening in your industry, in your part of the region and in the world. This will give you context to trends you should be aware of and things to consider as suspicious activity.

Keeping yourself updated on topics like anti-money laundering, terrorist financing is a great place to spend some time once a week, reading articles and staying aware.

Looking up fines that other MSBs have had recently is a great way to stay on top of activities you should look out for in your business. Learning from others mistakes is a great mindset for protecting your business, not just staying compliant.

The WSJ has a section titled “compliance”. This is a great resource for keeping track of current day activities and what to look out for in your business.

The bottom line is that you should want to be the best at being compliant, because it’s a huge component to the business you’re in. To be the best, you have to seek out knowledge and resources to get better and instill that mentality in all of your employees.

As we seek to be the best in what we do, we want to be one of those resources and extend that knowledge to you so you can grow wisely.

If you have questions about employee training, please reach out to our team.

Resources for Training:

Anti-Money Laundering – https://www.acams.org/en

https://www.fincen.gov/resources/advisoriesbulletinsfact-sheets/advisories

https://www.fincen.gov/news-room/enforcement-actions

Our ultimate goal with our MSB community is to be a resourceful partner in compliance. We want to see you succeed and see your customers succeed. In this article we’ll cover the very important topic of passing a state exam or an audit. We want to help you understand how to approach it and steps you can take to be successful.

Be Organized

This may seem at first like the simplest approach, but we see MSBs everyday who don’t have their business and paperwork in order. They don’t have foundational systems in which they run their business and it shows in their disorganization. Most of the time not having a formal process that your team can work from begins to disrupt all kinds of other aspects of your business.

Making the choice to get organized is of high value when it comes to passing any state exam or audit. Knowing you can put your hands on any documents that are requested is a good feeling and excellent way to know what is happening at any time in your business. Scrambling last minute to find information usually results in undue stress on you and your team and inevitably creates bigger problems as one event leads to another.

Be Aware of What’s Required

The great part of any state exam or audit is that it is not a mystery. Everything that is required of you is available online. If you want to build a process around a successful exam, take a look at the appropriate resources and prepare accordingly.

Below is the link to the FinCEN MSB Exam manual. This is what FinCEN uses when conducting an exam on a MSB. Studying this document is like getting a copy of the test before you take it.

https://www.fincen.gov/sites/default/files/shared/MSB_Exam_Manual.pdf

There are all the resources you need to comply with the agency who will be examining your business. The bottomline is that you and your team just have to do the front end work of studying them so you can organize your process around them.

Be Respectful

Having helped many MSBs for many years, we’ve seen the potential for some of them to not respect the position or authority of the examiner and the role they play in keeping the industry regulated. As an MSB, it is important for you to do your part in complying with the regulators.

Regulators are just normal people that put on their pants on one leg at a time, just like we do. So treating them with respect and not having a confrontational relationship with them typically leads to them not making you have a bad day. This is very similar to your interaction with a police officer. When you get pulled over, it’s better to just cooperate with their requests (license, registration etc) rather than being disrespectful.

In summary, our best advice is to do the right thing every day. Then it’s not going to feel like you’ve got two years worth of weight on your shoulders trying to get ready for an exam.

If you would like more information on this topic or any topic that is related to running a successfully compliant business, reach out to our BSA team at www.mysuretybank.com/msb.

This is the first of a new series of fictional case study articles. The business principles are applicable to all industries, not just the industry mentioned below.

Mike had spent years building his commercial construction company from the ground up. He took pride in his work, bidding on high-profile projects and assembling what he thought was a solid team. But as his company grew, so did his hiring challenges—especially when it came to leadership positions.

One project in particular—a multi-million dollar office complex—pushed his business to the edge. Under pressure to meet deadlines, Mike rushed to hire a new project manager, Tom, who came with an impressive résumé and glowing recommendations. But within weeks, cracks began to show.

Tom cut corners, ordered cheaper materials to save costs (without approval), and ignored safety protocols. Worse, he treated crew members poorly, causing skilled workers to quit mid-project. By the time Mike caught on, the damage was done. The project was behind schedule, client trust had eroded, and fixing Tom’s mistakes cost the company thousands.

Determined not to repeat the mistake, Mike changed his hiring approach. He thoroughly vetted new hires, conducted trial periods for leadership roles, and built a workplace culture that rewarded integrity and reliability. Within a year, his company had a team of dedicated leaders who took pride in their work—and it showed in their projects.

For businesses like Mike’s, hiring the right leadership isn’t just about filling roles—it’s about protecting the company's reputation, profitability, and long-term success.

A business can only succeed if its leadership is competent, ethical, and aligned with company values. A poor leadership hire can derail entire teams, weaken morale, and ultimately cost the company in lost productivity and damaged relationships.

The problem isn’t just finding someone with the right credentials. Many executives, managers, and directors look great on paper but fail to lead effectively. Worse, some take advantage of their positions, making decisions that benefit themselves at the expense of the company.

Avoiding these pitfalls requires a thoughtful hiring strategy that goes beyond skills and experience to assess character, leadership style, and long-term commitment.

When hiring for leadership roles, businesses should focus on finding ethical, capable, and accountable individuals. Here’s how:

Even the best leadership hire won’t stick around if they feel undervalued or unsupported. To keep strong leaders, businesses should:

Hiring and retaining the right leaders is just as critical—if not more so—than hiring the right employees. Leaders set the tone for company culture, influence productivity, and ultimately determine business success.

If your company has struggled with hiring leadership roles, it’s time to refine your hiring process, emphasize integrity, and invest in leadership development. By learning from mistakes—like Mike did—and implementing better hiring and retention practices, businesses can build a team of strong, ethical leaders who drive long-term success.

For more pratical information on hiring for a leadership position, check out this recent episode of the Expandable Show. https://www.youtube.com/watch?v=NtRezs5v4oA

In this article we want to answer the major questions surrounding proper employee training so you can use this as a tool to improve the performance of your business.

Why you should train your employees

Most mistakes that MSBs make in their businesses are directly related to their lack of employee training.

Many mistakes can be avoided, and your business doesn’t have to suffer by being held back. But it takes a little bit of time and energy invested into best practices to create an environment that is geared towards training.

We see some MSBs focusing their time and attention in other places too often which leaves their employees unsure about how to handle certain situations. The result can come in the form of fines, slowed growth, losing your MSB license and even losing their banking relationship.

Another major reason to train employees is to fully utilize your resources and assets. For example, you are using a software for check cashing. Are you using just the surface level features or are you using it to its fullest potential? This software offers a lot of features that can make your employees’ jobs much easier and can create efficiencies that map to profitability. This asset alone could bring improvements that impact your business tremendously in the short and long term.

Employee training should be held as a high priority and taken seriously. If so, the result is a smooth operation, less drag on resources and time spent fixing mistakes and less worry about being in business in the coming months or years.

Taking employee training seriously is the first step to sustainable growth in your MSB business. It’s the foundation of everything you do and the bedrock of your business.

How to train your employees

One of the four pillars of BSA is required employee training.

Naturally, if training is not considered a high priority in your business, employees will find ways to fulfill this requirement without becoming more knowledgeable or getting better in their role. People are generally going to take the path of least resistance when it is offered to them unless you are creating an environment with a higher standard.

Taking a basic test online to fulfill training requirements isn’t always going to achieve the desired result. You’re not doing training just to say you completed it. The purpose of completing the training is to stay compliant, get better and avoid costly mistakes that can put you out of business.

Besides completing a standardized test to confirm your knowledge of the subject, employee training best practices include several other factors. We’ve listed some of them here.

Stay up to speed on current events that are happening in your industry, in your part of the region and in the world. This will give you context to trends you should be aware of and things to consider as suspicious activity.

Keeping yourself updated on topics like anti-money laundering, terrorist financing is a great place to spend some time once a week, reading articles and staying aware.

Looking up fines that other MSBs have had recently is a great way to stay on top of activities you should look out for in your business. Learning from others mistakes is a great mindset for protecting your business, not just staying compliant.

The WSJ has a section titled “compliance”. This is a great resource for keeping track of current day activities and what to look out for in your business.

The bottom line is that you should want to be the best at being compliant, because it’s a huge component to the business you’re in. To be the best, you have to seek out knowledge and resources to get better and instill that mentality in all of your employees.

As we seek to be the best in what we do, we want to be one of those resources and extend that knowledge to you so you can grow wisely.

If you have questions about employee training, please reach out to our team.

Resources for Training:

Anti-Money Laundering – https://www.acams.org/en

https://www.fincen.gov/resources/advisoriesbulletinsfact-sheets/advisories

https://www.fincen.gov/news-room/enforcement-actions

Our ultimate goal with our MSB community is to be a resourceful partner in compliance. We want to see you succeed and see your customers succeed. In this article we’ll cover the very important topic of passing a state exam or an audit. We want to help you understand how to approach it and steps you can take to be successful.

Be Organized

This may seem at first like the simplest approach, but we see MSBs everyday who don’t have their business and paperwork in order. They don’t have foundational systems in which they run their business and it shows in their disorganization. Most of the time not having a formal process that your team can work from begins to disrupt all kinds of other aspects of your business.

Making the choice to get organized is of high value when it comes to passing any state exam or audit. Knowing you can put your hands on any documents that are requested is a good feeling and excellent way to know what is happening at any time in your business. Scrambling last minute to find information usually results in undue stress on you and your team and inevitably creates bigger problems as one event leads to another.

Be Aware of What’s Required

The great part of any state exam or audit is that it is not a mystery. Everything that is required of you is available online. If you want to build a process around a successful exam, take a look at the appropriate resources and prepare accordingly.

Below is the link to the FinCEN MSB Exam manual. This is what FinCEN uses when conducting an exam on a MSB. Studying this document is like getting a copy of the test before you take it.

https://www.fincen.gov/sites/default/files/shared/MSB_Exam_Manual.pdf

There are all the resources you need to comply with the agency who will be examining your business. The bottomline is that you and your team just have to do the front end work of studying them so you can organize your process around them.

Be Respectful

Having helped many MSBs for many years, we’ve seen the potential for some of them to not respect the position or authority of the examiner and the role they play in keeping the industry regulated. As an MSB, it is important for you to do your part in complying with the regulators.

Regulators are just normal people that put on their pants on one leg at a time, just like we do. So treating them with respect and not having a confrontational relationship with them typically leads to them not making you have a bad day. This is very similar to your interaction with a police officer. When you get pulled over, it’s better to just cooperate with their requests (license, registration etc) rather than being disrespectful.

In summary, our best advice is to do the right thing every day. Then it’s not going to feel like you’ve got two years worth of weight on your shoulders trying to get ready for an exam.

If you would like more information on this topic or any topic that is related to running a successfully compliant business, reach out to our BSA team at www.mysuretybank.com/msb.

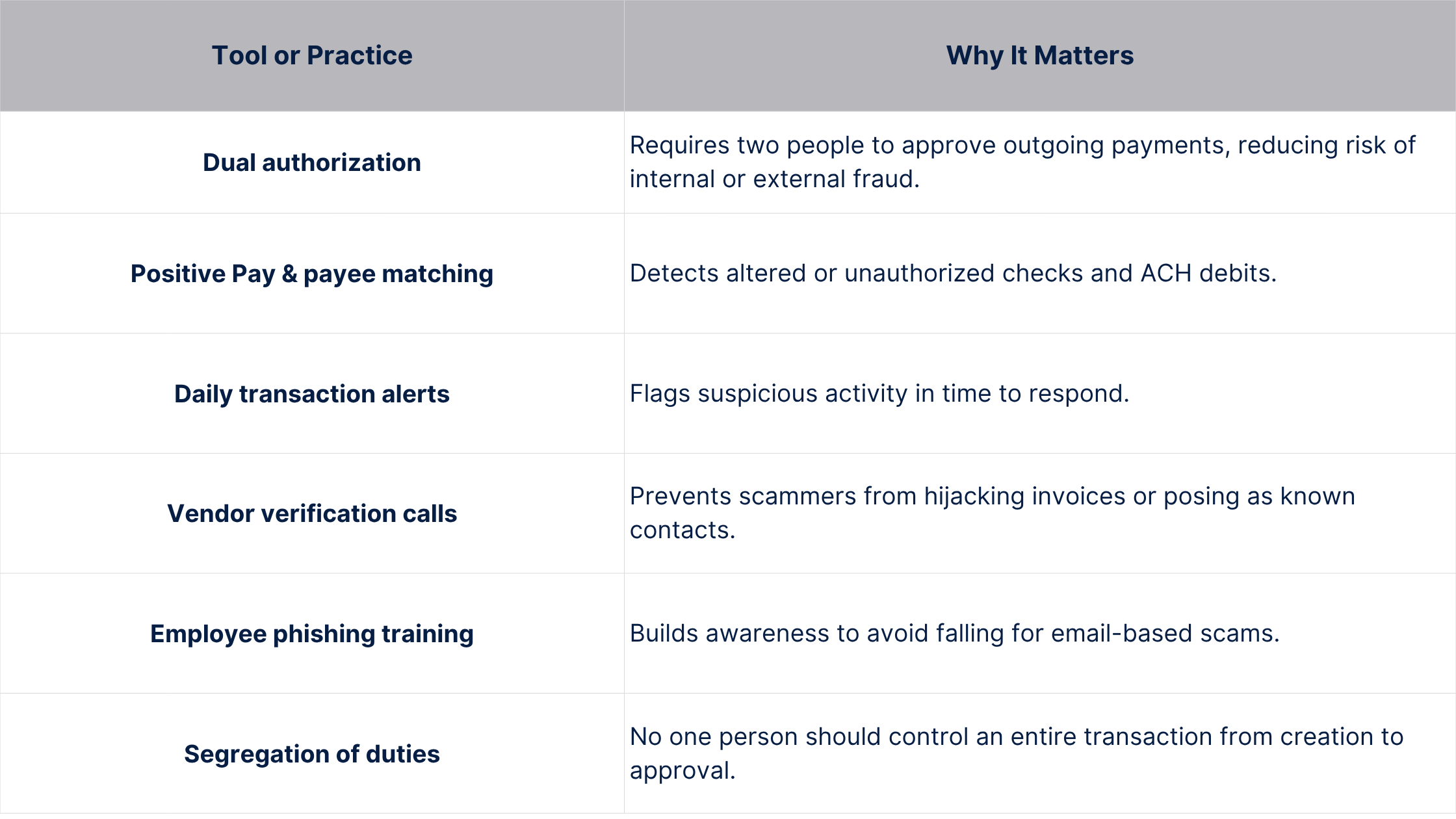

At first glance, a checking account is a checking account. Money comes in, money goes out, and you check the balance when you need to. But the day you start running a business, the rules change, because the risk changes. Business accounts aren’t just “bigger” consumer accounts. They typically handle more transactions, more users, more payment types, and more moving parts.

There’s another key difference many owners don’t realize until it’s too late: business accounts generally do not have the same level of consumer protections that consumer (personal) accounts do. When something goes wrong, the process, timelines, and potential liability can look very different. That’s why fraud prevention for businesses isn’t optional. It’s operational.

Consumer (personal) accounts are usually simpler:

Business accounts are different by design:

And because business accounts are treated differently than consumer accounts, the responsibility to monitor activity and catch issues early often rests more heavily on the business.

Most business owners are busy. Delegating bookkeeping is smart, because your time is valuable. But delegation without visibility is where risk grows, especially when one person has end-to-end control.

Internal fraud often looks like:

It’s rarely dramatic at the beginning. It’s usually quiet, incremental, and designed not to be noticed.

Consider Lisa, who owns a growing medical practice. She hired a bookkeeper to “handle the finances” and assumed monthly reports were enough. Lisa rarely reviewed actual transactions unless something felt off.

Over time, the bookkeeper began issuing checks to a vendor that sounded legitimate. The amounts were small—$180 here, $250 there—coded as routine office supplies. The practice was busy, revenue was strong, and nothing looked “wrong” at a high level.

Six months later, Lisa’s accountant flagged unusual expense patterns during a quarterly review. By then, the total loss wasn’t a rounding error. It was meaningful, and the cleanup took time, created stress, and required uncomfortable conversations. The hardest part wasn’t just the money; it was realizing the problem could have been caught early with simple, consistent oversight.

You don’t need to become your own bookkeeper. You just need a rhythm of review that helps you spot unusual activity quickly, especially because business accounts don’t always come with the same consumer-style protections.

Try these straightforward habits:

Strong habits matter, but systems are what help you scale safely. Depending on your business, ask about tools such as: